At the end of the day, I think we all have the same goal: get super rich, so you can tell your seventh grade math teacher that you DIDN’T need to know Algebra to succeed.

So I thought I’d write about making money by investing. Unfortunately, it involves math.

Here’s what we’re talking about today:

Compound Interest (an ‘interesting’ topic),

Stocks, Bonds, and Cash - Oh My!,

Alt(ernatives) Rock, and finally

How to Get Filthy Stinkin’ Rich (by building more efficient portfolios).

Before we begin, there are some things you should know.

First, the people we work with never have a main goal of “more money.” Money only helps you achieve your goals; it should never be the goal itself. Thus, improving the efficiency of the portfolios is aimed at getting more use out of the money you have - not just accumulating more.

Second, some of the strategies I discuss in this article can have adverse effects if implemented improperly. Please don’t try this at home without first doing much more research. Better yet, engage a professional who can help you determine when and if the strategies discussed are right for you.

Third, and most importantly, this article is for educational purposes only, and is not advice (not to use the strategies, not to use the funds, not to invest or not to invest in general). If you’d like to discuss this content, please reach out to me or someone on my team. The charts show investment benchmarks for illustrative purposes, and these benchmarks may not necessarily be the benchmarks used to create portfolios at Preece Financial Services. Also, all return data is calendar year return data from Yahoo.

Man, what a drag - all those disclosures. Let’s get into it!

Compound Interest (an ‘interesting topic’)

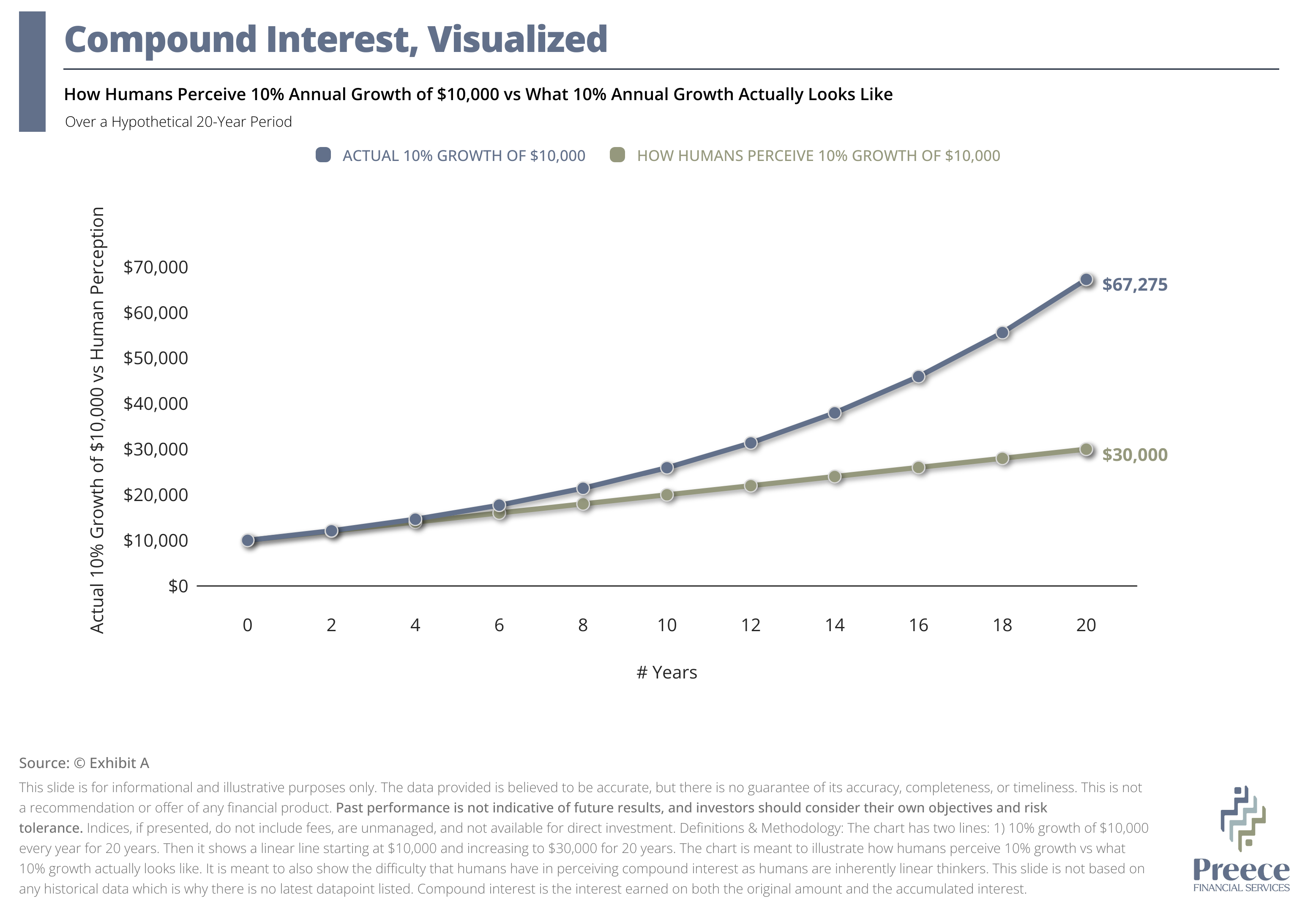

As humans, we aren’t great at comprehending compound interest. Think about it - how often did our ancestors have to do any math beyond basic addition and subtraction? As such, we tend to think linearly while compound interest grows exponentially. See below for an example.

The takeaway? Compound interest is the mechanism by which your money can grow faster than you realize. Here’s a shortcut on the math: The Rule of 72.

Say you can make 6% per year on your investments, and all of that is getting reinvested. If you take 72 and divide it by 6, that will give you an idea of how many years it will take your initial investment to double - 12 years (72/6=12).

Now, let’s say you figure you can average 10% per year. Then your initial investment should double in about 7 years (72/10=7.2).

The thing is, “compound interest” is a bit of a misnomer. The truth is that most of your returns if you’re investing come from either price growth or dividend payments, and most investments that pay interest will keep you toward the left side of this chart.

Stocks, Bonds, and Cash - Oh My!

Once you understand compound interest (returns), the next question is almost always “how do I get me some compound interest (returns)?” And it’s simple… kind of.

You invest!

The main three assets that people invest in are stocks, bonds, and cash.

“But what about real estate?”

Ah, yes, real estate. The focus of this article is building portfolios in your brokerage account. Real estate can be a great investment, but it’s often not a great fit for holding in a brokerage account. For now, let’s start with cash.

“Cash is king!” - common, misleading phrase. Cash is important to have for short-term needs. But if we’re talking long-term, you’re likely to have your purchasing power eroded by inflation. Sure, there’s little risk in the value of your cash changing in the short term, so it’s “safe.” However, holding cash for decades has historically been a losing bet.

So, make sure you have enough cash for emergencies and upcoming expenses, but with what cash you do hold, be sure to utilize high yield savings accounts, CDs, or treasury bills to earn low-risk, low-reward interest.

Now, onto stocks and bonds.

If you go to your parents’ financial advisor, they might tell you something like this:

“Take 100 and subtract your age. That’s how much of your portfolio should be in the stock market.”

This is a silly rule of thumb, and I don’t use it, but the reason it exists is because stocks are more volatile (meaning they go up and down a lot), and bonds are less so. As you get closer to spending the money (i.e. retirement), you want your portfolio to be more conservative. Check out this chart laying out drawdowns in stocks vs. drawdowns in bonds since 1990.

So you can see that, typically, in bad years for bonds, it really wasn’t all that bad, while in bad years for stocks, it can get pretty ugly.

“Well, why would I invest in stocks then?”

Thank you! Really, thanks for asking! It’s like you knew what I wanted to say next.

We invest in stocks because with that greater risk, comes greater reward (higher returns). At least, that’s the case historically speaking. Could that change? Of course. But over the long run, the general consensus is that we will expect higher returns from stocks than from bonds because of the greater risk. Here’s a little context:

More stocks, more risk, higher returns.

More bonds, less risk, lower returns.

But what if I told you there’s another category?

Alt(ernatives) Rock

What are alternatives?

Really, they’re any investment that doesn’t fall neatly into the stocks, bonds, and cash we’ve already covered. We’re going to talk about the kind of alternatives that are relatively easy to add to your investment portfolio, but they often include real estate, commodities, precious metals, collectibles, art, and really anything else that can be held as an investment.

When considering adding alternative exposure, I ask a few questions:

- What’s the cost? All investments have a cost. All things considered, we want the cost to be relatively low.

- Do we expect positive returns? We typically want to make money. Yes, you can make the case for a diversifying asset that has negative returns, but it’s tough to hold onto.

- Does it have low/negative correlation to the rest of the portfolio? These assets tend to have lower returns than stocks, so the ONLY benefit we get from adding them to the portfolio is that they zig when the rest of our investments zag.

- Is their volatility similar to that of the stock market? We want something that has a high probability of having a high return when stocks are down. That means it needs to be volatile and prone to high swings.

To diversify stock exposure, I focus on commodities, gold, and high duration US Treasury bonds. Yeah, we already talked about bonds. These bonds are different, kind of. Confusing, I know.

We can run back tests to see how these asset classes may have worked in different market cycles. For instance, a fund that holds high duration US treasury bonds (TLT) had a return of 33.92% in 2008 when an S&P 500 fund (SPY) had a return of -36.81%. If you held both in equal amounts, your return that year would have been only slightly negative. Better yet, if you sold your gains in TLT to buy SPY (we call this “rebalancing”), you would see a huge comeback in 2009 when almost the exact opposite happened (SPY was up 26.37% and TLT was down 21.80%).

So, let’s say you started with $10,000.

| SPY | TLT | 50/50 Un-rebalanced | 50/50 Rebalanced | |

|---|---|---|---|---|

| 2008 | 6,319 | 13,392 | 9,856 | 9,856 |

| 2009 | 7,985 | 10,473 | 9,229 | 10,081 |

| Worst | -36.81% | -21.80% | -6.36% | -1.44% |

| Best | 26.37% | 33.92% | -1.44% | 2.28% |

Even though investing in TLT resulted in the best overall return in those two years, you had to sit through a 21.80% drawdown in the second year. Painful.

Notably, diversification WITHOUT rebalancing isn’t all that helpful. Note that the un-rebalanced portfolio was actually negative in both years. Here’s something to remember: If you don’t rebalance your portfolio, it will almost certainly get riskier and more concentrated over time as the higher-risk positions outgrow the lower-risk positions, thus taking up more of the account.

After 2008, the un-rebalanced portfolio was actually 32% stocks and 68% bonds, while the rebalanced portfolio would have placed trades to get back to 50% stocks and 50% bonds.

At this point, I do hear you groaning: “Why are we doing all this math?”

Good question. Let’s stop with that. TO THE POINT!

With that pretty little table, you can see the benefit of diversification and how rebalancing improves those benefits even with two assets that tend to be uncorrelated (meaning they do different things at different times).

Now, what if we did it with MORE assets that are uncorrelated?

Enter alternatives.

For our purposes today, we’re going to use GSG, which is a fund that tracks a commodities index. There are other alternatives out there aside from commodities (real estate, precious metals - technically commodities - stock-based strategies, cryptocurrency, etc.), but commodities will do for today. Unfortunately, we’re going to do more math.

If you looked at that last table and thought “but what about when stocks and bonds correlate, like they did in 2022?” congratulations, you get a cookie (you are responsible for shipping, however). In 2022, stocks and bonds were BOTH down by double digits. This surprised a lot of people, and it was painful to watch.

Let’s look at the period from 2020-2023 with SPY, TLT, GSG, a 50/50 SPY & TLT portfolio, and a 35/35/30 SPY, TLT, & GSG portfolio (both rebalanced). I’m just going to put the percentages in there this time.

| SPY | TLT | GSG | 50/50 | 35/35/30 | |

|---|---|---|---|---|---|

| 2020 | 18.37% | 18.15% | -23.94% | 18.26% | 5.60% |

| 2021 | 28.75% | -4.60% | 38.77% | 12.08% | 20.08% |

| 2022 | -18.17% | -31.24% | 24.08% | -24.71% | -10.07% |

| 2023 | 26.19% | 2.77% | -5.51% | 14.48% | 8.48% |

| Total | 57.37% | -20.35% | 23.75% | 14.25% | 23.71% |

| Worst | -18.17% | -31.24% | -23.94% | -24.71% | -10.07% |

| Best | 28.75% | 18.15% | 38.77% | 18.26% | 20.08% |

What an interesting 4-year period. In each of these 4 years, at least one of these three assets moved in the opposite direction of the other two.

The really interesting piece is the comparison of the 50/50 (SPY/TLT) portfolio and the 35/35/30 (SPY/TLT/GSG) portfolio.

We added a position (GSG) that had a total return of 23.75% and a worst year of -23.94% over that timeframe.

This increased the total return of the portfolio to 23.71% from 14.25% while improving the worst year from a loss of -24.71% to a loss of -10.07%.

So adding GSG, which was more volatile than the 50/50 portfolio, actually reduced risk AND increased returns over that time period. This is the real value of true diversification.

Of course, you might look at this and think “man, SPY would have been the way to go here.” And of course, your hindsight is 20/20. But at the beginning of 2023, economists had famously forecast a 100% probability of a recession. In 2020, a large portion of us thought the world was ending and taking the economy down with it.

This is kind of the downside of diversification - you have to reduce exposure to your highest performing positions in order to get the diversification…

Or do you?

How to Get Filthy Stinkin’ Rich (by building more efficient portfolios)

I’m going to start this with another caveat - you don’t get rich by building more efficient portfolios. You get rich by investing more. That said, better returns can’t hurt, right?

So we know by now that diversification is the key to lower risk, and that’s achieved by adding assets to a portfolio that:

- Are uncorrelated (don’t necessarily move in the same direction as your other investments in any given year), and

- Are about as volatile as your other investments.

You might be thinking, “diversification is great and all, but I really don’t want to reduce my exposure to stocks just to be more diversified.”

Well, there’s a potential solution: leverage.

What’s leverage? In essence, it’s borrowing money to invest. There is ALWAYS a cost to leverage, so it’s important to use it wisely.

Let’s illustrate keeping 60% exposure to the S&P 500 in that last 4-year period by adding 30% to SSO (a 2x S&P 500 ETF) instead of reducing our exposure to 35% in SPY.

| SSO | TLT | GSG | Original 35/35/30 | Leveraged 30/35/35 | |

|---|---|---|---|---|---|

| 2020 | 21.53% | 18.15% | -23.94% | 5.60% | 4.43% |

| 2021 | 60.57% | -4.60% | 38.77% | 20.08% | 30.13% |

| 2022 | -38.98% | -31.24% | 24.08% | -10.07% | -14.20% |

| 2023 | 46.66% | 2.77% | -5.51% | 8.48% | 13.04% |

| Total | 74.64% | -20.35% | 23.75% | 23.71% | 31.80% |

| Worst | -38.98% | -31.24% | -23.94% | -10.07% | -14.20% |

| Best | 60.57% | 18.15% | 38.77% | 20.08% | 30.13% |

Let’s first note that SSO does not have a total return that is double that of SPY - this is due mainly to volatility drag. SSO targets 2x the return of SPY on a daily basis, which causes the return on an annual basis and over time to deteriorate below 2x the total return.

If you invest $100 in SPY, and it’s up 10% and then down 10%, your $100 goes to $110, then down to $99, resulting in a return of -1%.

If you invest that same $100 in SSO, your returns will be 20% and then -20%, so your $100 will go up to $120 and then down to $96, resulting in a return of -4%.

This is why we don’t directly invest in leveraged ETFs for long periods of time; however, rebalancing with uncorrelated assets helps to minimize volatility drag, and can allow us to build more efficient portfolios, improving returns over time while still benefitting from diversification.

If you’d like to do more research on this topic, it’s commonly referred to as “portable alpha.” But once again, be careful. Anytime leverage gets involved, it’s easy to make costly mistakes.

Hi, I’m Austin Preece, CFP®, EA. I’m a fee only financial planner and tax advisor with Preece Financial Services. We have locations near Madison and Eau Claire, Wisconsin. Sign up to be notified via email about future blog posts, so you don’t miss any timely, educational posts.

Preece Financial Services is a DBA of Wealth Planning Advisors LLC, which is an RIA registered in Wisconsin, Minnesota, and Arizona. Tax preparation and planning services as well as bookkeeping and payroll services are offered through Preece Accounting Services LLC.

Austin Preece, CFP®, EA

Financial Planner

Austin is a fee-only financial planner and tax advisor based near Madison, Wisconsin, working virtually with clients across the US. He specializes in comprehensive financial planning, investment management, and tax planning strategies. Haven't found the answers you were looking for in the blog? Reach out!

Related Articles

Can a Financial Planner Boost Your Investment Performance?

Can a Financial Planner Boost Your Investment Performance? explained by financial experts. Preece Financial Services shares proven strategies and insigh...

4 Guidelines for Building Portfolios

4 Guidelines for Building Portfolios explained by financial experts. Preece Financial Services shares proven strategies and insights. Click to read the ...